"One of the UK's leading specialists in financial mis-selling…"

The Times

If you’ve lost money on a mis-sold investment, strict deadlines could affect your right to compensation. Here’s what you need to know — and how to check if you’re still eligible.

Many investors only realise years later that the advice they received was unsuitable, high-risk, or misleading. By then, they worry it may be too late to make a claim.

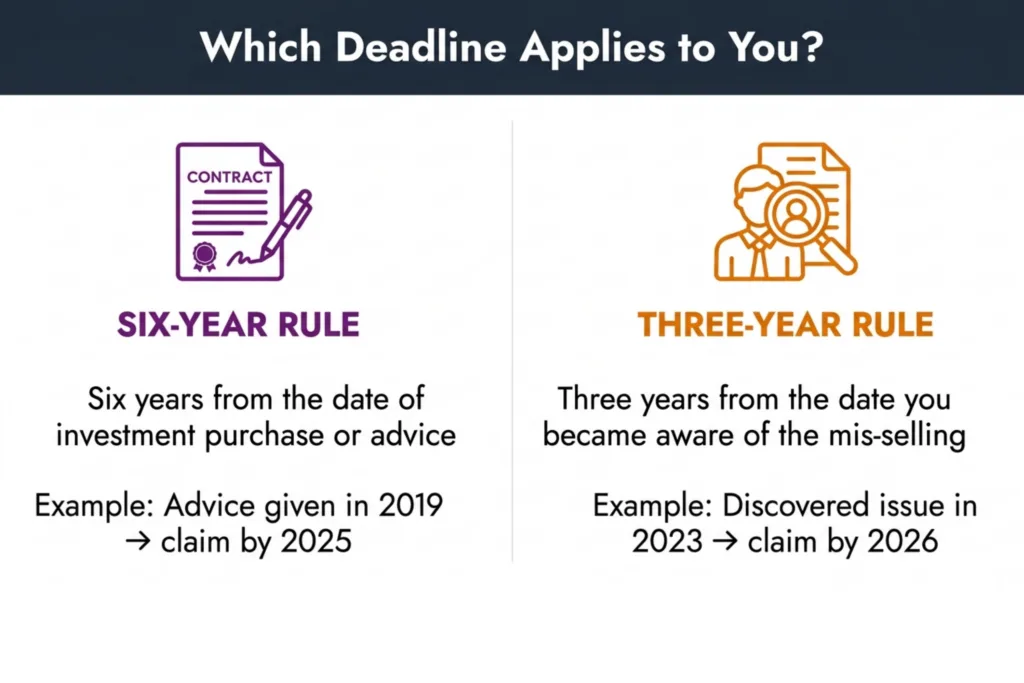

In England and Wales, strict legal deadlines apply to investment mis-selling claims. These are known as limitation periods. If you miss them, you may lose your right to claim compensation entirely.

However, time limits are not always straightforward. The ‘six-year rule’ and ‘three-year rule’ can overlap. In some cases, the deadline may start later than you think, particularly if you only recently became aware of the problem.

In our experience, many clients contact us assuming they are already too late to make a claim, because their investment was made more than six years ago. However, after reviewing their documents, we often find that the ‘three-year ‘awareness rule applies instead.

A common pattern involves investors who only realised the true risk of a product after retirement planning discussions or regulatory warnings. In several cases, ongoing adviser reviews can restart the limitation start date. These situations demonstrate that time limit concerns should always be assessed individually, rather than assumed.

This guide explains how the financial mis-selling time limit works, when the clock starts running, and whether you may still be in time to claim.

Most investment mis-selling claims are governed by the Limitation Act 1980. This law sets the primary investment claim time limit for bringing court proceedings in England and Wales.

For claims founded on negligence, breach of statutory duty or breach of contract, you have six years from the date the advice was given, regulatory rules were breached, or the investment was sold to start a court claim.

The clock usually begins when:

This rule applies even if you did not realise the advice was unsuitable at the time. Losses occurring later do not reset the six years.

If more than six years have passed, a claim founded in negligence only may still be possible under the three-year rule.

Alternatively, you have three years from the date you first knew (or should reasonably have known) that you had suffered a loss and could make a claim.

The three-year rule is particularly important where investors only discover relevant facts at a later date, for example:

Example: An investor who purchased a scheme in 2015 but only learned in 2023 that it was unsuitable may still have until 2026 to bring a claim.

Consider this simplified timeline:

Under the six-year rule, a court claim would appear out of time in 2021. However, if the investor only became aware in 2024 that the investment’s projected profit/return on equity had turned negative, the three-year rule may allow a claim until 2027.

Importantly, though, a court may still ‘fix’ the investor with knowledge in 2020, despite the investment manager’s excuses. It depends on what the court thinks the investor ought to have known and whether it thinks they should have been prompted to investigate further. This would mean that the three-year rule would have expired in 2023.

This is why it is important to seek early legal advice; the test is not just what the investor knew, but also what the court thinks they ought to have known. The key difference is that the six-year rule looks at when the advice was given, whilst the three-year rule looks at when the investor knew the advice was wrong.

The most disputed issue in many claims is when the limitation period actually began.

The clock may start from:

The date of actual financial loss is not always decisive. What matters is when you knew, or ought reasonably to have known, that the loss may have resulted from unsuitable advice.

Courts and the Financial Ombudsman Service (FOS) look at factual evidence to decide when awareness arose.

Common triggers include:

Important: Poor performance alone does not automatically start the clock. Awareness requires understanding that the advice itself may have been unsuitable, not simply that markets fell.

If your adviser reassured you that the investment remained appropriate, this may delay the awareness date.

In a recent case, our client’s claim was found to have been brought in time despite the fact that the investment had been made more than six years ago. It was because they could only have been expected to begin investigating matters once they were on notice that the investment was predicted to make a loss.

The investment claim time limit is not always fixed. Certain legal exceptions may extend or postpone it.

These exceptions are highly fact-specific and often misunderstood.

If your adviser provided continuing reviews, portfolio updates, or ongoing recommendations after the initial sale, the limitation period may run from when that advisory relationship ended. Fresh advice to retain or maintain an unsuitable investment can amount to a new act of negligence.

This often arises in:

Where unsuitable advice continued for years, the limitation clock may begin later than the original purchase date. Each fresh review, if negligent, can be said to create a new cause of action.

Under Section 32 of the Limitation Act 1980, the limitation period does not begin until you discover deliberate concealment or fraud.

This may apply where an adviser:

Deliberate concealment requires more than simple oversight. There must be evidence that material facts were intentionally withheld.

The Supreme Court considered the meanings of the words “deliberate” and “conceal” in Canada Square Operations Ltd v Potter [2023] UKSC 41.

It was held that “conceal” means to keep information secret, either by taking active steps to hide it or by failing to disclose it, whether or not there is an obligation to disclose, and that “deliberate” is akin to intentional and does not include recklessness.

| Concealment | Non-Disclosure |

|---|---|

| Intentional | Accidental |

| Material conflict | Minor oversight |

| Affects decision | Administrative issue |

Where a client was vulnerable, elderly, or heavily reliant on an adviser, courts may accept that awareness arose later.

The Financial Ombudsman Service also applies a fairness-based approach and may allow complaints outside strict time limits where vulnerability or exceptional circumstances delayed action.

Each case depends on the individual’s knowledge and circumstances.

| Factor | Financial Ombudsman Service (FOS) | Court Claim |

|---|---|---|

| Time Limit Rules | 6 years from sale or 3 years from awareness. FOS has discretion to extend in rare cases. | Strict 6-year limit (Limitation Act 1980) or 3 years from date of knowledge. |

| Complexity | Simple, less formal process. | Legal procedure, evidence, and legal representation required. |

| Typical Use Case | Claims under £375,000 or if the adviser is still authorised. | Larger or complex claims, or where FOS isn’t suitable. |

| Outcome | Binding on firms if accepted by the claimant. | Court judgment enforceable. |

Court claims are governed by the Limitation Act.

Complaints to the Financial Ombudsman Service follow separate DISP rules. In most cases, you must complain within:

Firms can raise a time bar, but the Ombudsman may consider whether it was reasonable for you not to complain earlier.

The key point: even if the court limitation has expired, a FOS complaint may still be possible.

Time limits can be affected by the structure of the investment and the type of advice given.

Unregulated Collective Investment Schemes (UCIS) often lack transparent valuations and may only reveal problems years later.

Illiquidity, suspended withdrawals, or regulatory warnings frequently mark the first clear sign of unsuitability.

In such cases, the three-year awareness rule may start when those warning signs became apparent, not at the original purchase date.

Pension cases often involve multiple potential starting dates.

The clock may run from:

You may have separate claims for pension transfer advice and for the selection of high-risk investments within the pension.

Many investors only discover problems when approaching retirement and realise projected income cannot be met.

We often find that a potential matter may have several ‘trigger points’ for limitation. In a pension transfer case, for example, the original transfer advice may have been negligent, and then subsequent investment advice may form a second claim.

It is important to speak to an expert about the different types of claims that might be possible to maximise your potential recovery.

Standard regulated products such as ISAs and investment bonds generally follow the standard six-year and three-year rules.

However, issues arise where:

Even mainstream products can be mis-sold if the advice was fundamentally unsuitable.

Not sure whether you’re still within the deadline to claim for a mis-sold investment? Take a quick self-check below. If you answer “yes” to any of these, you may still be able to recover compensation.

| Question | If Yes |

|---|---|

| Has it been less than 6 years since you were sold or advised on the investment? | You’re likely within the standard time limit. |

| Did you only realise the investment was unsuitable or mis-sold in the last 3 years? | You may qualify under the “three-year rule.” |

| Were you given ongoing reviews or advice after the initial sale? | The time limit may run from when the advice relationship ended or the last review took place. |

| Have you recently discovered hidden fees, misleading information, or adviser concealment? | Time limits may be paused due to concealment. |

| Did your adviser fail to explain the risks or your options clearly? | This may support an exception to the standard time limit. |

| Have you experienced losses from a high-risk, unregulated, or complex investment? | These often fall within the scope of mis-selling claims. |

| Were you pressured into making a quick decision or told your money was “safe”? | This can indicate unsuitable or misleading advice. |

Even if none clearly apply, the limitation law is technical. Multiple pieces of advice, complex structures, or later discoveries can change the analysis.

Do not assume it is too late without reviewing your timeline carefully.

At Neglect Assist, we specialise in investment mis-selling claims and regularly navigate complex limitation issues. Time limits should never be a barrier to seeking justice, and our experience with these cases means we can often identify routes to compensation that other firms might miss.

Our approach includes:

For eligible cases, we offer No Win, No Fee representation.

Limitation disputes are often technical and heavily contested. Early legal assessment improves your position and preserves evidence.

Even if your investment was made many years ago, you may still be within the legal window to claim. The financial mis-selling time limit depends on when you became aware of unsuitable advice, not just when you signed the paperwork.

Many successful claims initially appear out of time until a detailed review reveals a later awareness date or an applicable exception.

Your eligibility depends on the specific facts of your case. Assumptions about deadlines can be misleading. Speak to one of our specialists if you’re not sure if you have a valid claim.

Answer a few quick questions and request a free callback. Our team will contact you for a no-obligation chat and explain the next steps.

“Losses alone do not start the limitation clock. What matters legally is when the investor knew, or reasonably ought to have known, that the loss may have resulted from negligent advice. In many cases, advisers continue providing reassurances for years, which can significantly affect the timeline.”

You may still claim under the three-year awareness rule if you only recently discovered the mis-selling. Concealment, ongoing advice, or vulnerability may also delay the start of the limitation period. Additionally, the Financial Ombudsman Service may consider complaints outside standard time limits where it was reasonable for you not to have complained earlier. Do not assume that passing six years automatically prevents action.

Yes. Compensation may still be available. Most advisers carry Professional Indemnity Insurance that covers past advice even after a firm closes. If the firm is insolvent or unable to pay, you may be able to claim through the Financial Services Compensation Scheme, which can compensate eligible claimants up to statutory limits. Time limits still apply, so early action is important.

Poor performance alone is not mis-selling. Mis-selling occurs where advice was unsuitable, risks were not explained, conflicts were hidden, or recommendations did not match your financial situation. An investment can be profitable yet still mis-sold if it exposes you to inappropriate risk. The key question is whether you would have invested had you been given full and proper information.

You need to identify:

Gather:

Awareness requires knowledge that the loss may have resulted from negligent advice, not simply market decline. A detailed timeline review is often necessary to determine the correct starting point.

Tim qualified as a solicitor in 2011 and has substantial experience handling professional negligence, financial mis-selling and fraud-related claims, including complex group actions involving systemic mis-selling.

You do not need legal representation to make a financial services claim. You can complain yourself at no cost and under FCA rules, the financial services provider must provide a response. If you feel this is unsatisfactory, you can complain to the statutory redress bodies, the FOS and FSCS who can award you compensation. This is a free service.

The information appearing within this website does not constitute legal advice and is provided for general information purposes only. No warranty, whether express or implied, is given in relation to such material, and we do not accept any liability for reliance on it.

Neglect Assist is a trading style of Wixted & Co Solicitors which is authorised and regulated by the Solicitors Regulation Authority (SRA) A copy of the SRA handbook can be obtained from www.sra.org.uk. Wixted & Co Solicitors, 57 Putney Bridge Road, London SW18 1NP.

Registered number 06243291. VAT number 788 6929 41.

© 2025 Wixted & Co Solicitors